Have you received a Payment Order for overdue loans? Here's how to freeze your loans!

NEWS

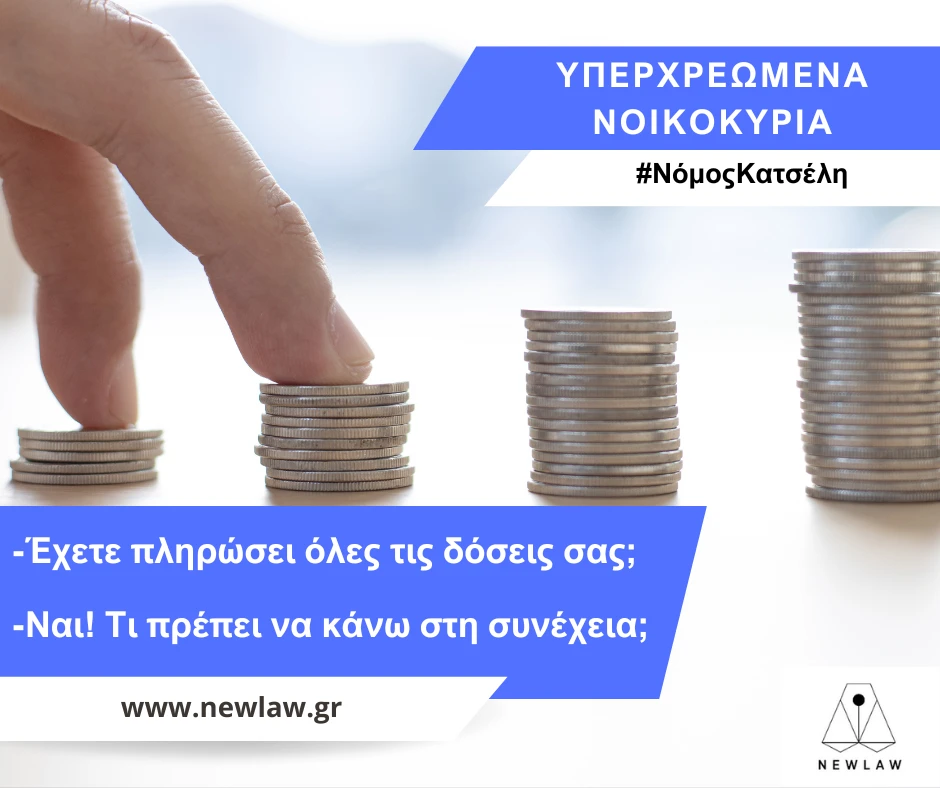

Have you been included in the Katseli Law and have you paid all the installments of your debt settlement? What do you need to do to be definitively discharged!

Many Greek citizens were included in the protective framework of Law 3869/2010 (also known as the Katseli Law). Income scarcity, high interest rates, particularly on consumer credit, and aggressive credit promotion practices were some of the factors that led thousands of citizens to over-indebtedness [1]. Unfortunate calculations and forecasts, combined with the absence of an advisory support institution for households facing financial problems, rapidly led to what we call "over-indebted households." The legislator addressed this situation by enacting Law 3869/2010 (the Katseli Law), based on the constitutional provisions of Article 2 paragraph 1 and Article 5 paragraph 1 of the Constitution, as the State is primarily responsible for respecting the dignity of every individual and for taking positive measures that strengthen and lead to the individual's reintegration into the economic and social life of the country.

Therefore, a multitude of Greek citizens, starting as early as December 2010 (Article 19 paragraph 2 and Article 4 paragraph 1 of Law 3869/2010), filed applications before the locally competent Court of First Instance (Eirinodikeio) with the aim of being included in the protective framework of the law. The basic negative prerequisites for their inclusion in the favorable regime of Law 3869/2010, according to Article 1, were the absence of merchant status and their non-fraudulent descent into a general and permanent inability to meet overdue monetary obligations. With the applicant's inclusion in the protective scope of Law 3869/2010, their overdue monetary debts were regulated by a court decision, which aimed to maintain a balance between the vulnerable debtor-borrower and the creditors.

The aim and hope of all debtors-borrowers was and is their final discharge from all their overdue – now regulated – monetary debts. However, this discharge could not occur automatically upon their inclusion in the protective scope of Law 3869/2010. For this precise reason, the related request, often combined with the application brief under Article 4 paragraph 1 of Law 3869/2010, was rejected as prematurely filed (i.e., as legally unfounded).

For the discharge of a debtor who managed to be included in the protective scope of Law 3869/2010, the regular payment of monthly installments to their creditors, as determined by the court decision, is a prerequisite. Anyone who has paid off their creditors in the manner prescribed by the court decision (e.g., paid 240 monthly installments of 25 euros to the credit institution according to the court decision) is entitled to file a discharge application under Article 11 paragraph 1 of Law 3869/2010 before the locally competent Court of First Instance, under the procedure of voluntary jurisdiction (Articles 739 et seq. of the Hellenic Code of Civil Procedure), which will confirm and certify the debtor's discharge from all their overdue monetary obligations.

This is an extremely important court decision, as it is the one that finally "removes" the "debtor" label from the vulnerable borrower-debtor. It is the court that issues and publishes a judicial decision that has the characteristics of a "proof of payment" that can be asserted against all creditors for the overdue monetary debts that were regulated by the initial decision that ruled on the inclusion of the then vulnerable borrower-debtor in the protective scope of Law 3869/2010.

Additionally, because it is very likely that the debtors' claims have been transferred from the credit institutions (e.g., anonymous banking companies) to Loan and Credit Acquisition Companies (Funds) and their management has been assigned to Loan and Credit Management Companies, this specific discharge application under Article 11 paragraph 1 of Law 3869/2010 is deemed necessary and imperative as the identity of the claim holder changes. However, with the favorable decision of the locally competent Court of First Instance that handles the discharge application under Article 11 paragraph 1 of Law 3869/2010, the debtor ceases to be called a debtor, and any extrajudicial or judicial demand they receive from a Fund can be countered by presenting the Court of First Instance's decision certifying their discharge from all their monetary obligations.

For more information, if you were included in the protective scope of Law 3869/2010 (Katseli Law) and are reaching the end of your monthly installment payments or have paid the full number of monthly installments to the credit institutions according to the court decision, then it is absolutely imperative for the aforementioned reasons to immediately proceed with a discharge application under Law 3869/2010. To schedule an appointment to resolve your case, you can call the specialized law firm NEWLAW on all working days from 8:00 a.m. to 5:00 p.m. at the telephone numbers 2310 551 501 and 2310 261 501.

[1] See the Explanatory Memorandum of Law 3869/2010.

The Most Read

How to Help Your Loved Ones If They Have Diminished Mental and/or Physical Capacity

Know Your Rights: Warranty for Electrical Appliances & Goods